India’s Climate Tightrope: What the Approved NDCs Mean for Startup Builders

No country has been asked to do what India is being asked to do. Home to over 1.45 billion people, it is the world’s sixth largest economy by GDP and the world’s third largest greenhouse gas (GHG) emitter. It is also the 9th most affected country by the adverse consequences of climate change. The climate crisis is no longer a future problem for India. Between January and November 2025, India experienced extreme weather events on 331 of 334 days, or nearly one event every single day. In the past three decades (1995-2024), climate change induced extreme weather events have affected nearly 1.3 billion people and resulted in economic losses of close to USD 170 billion.

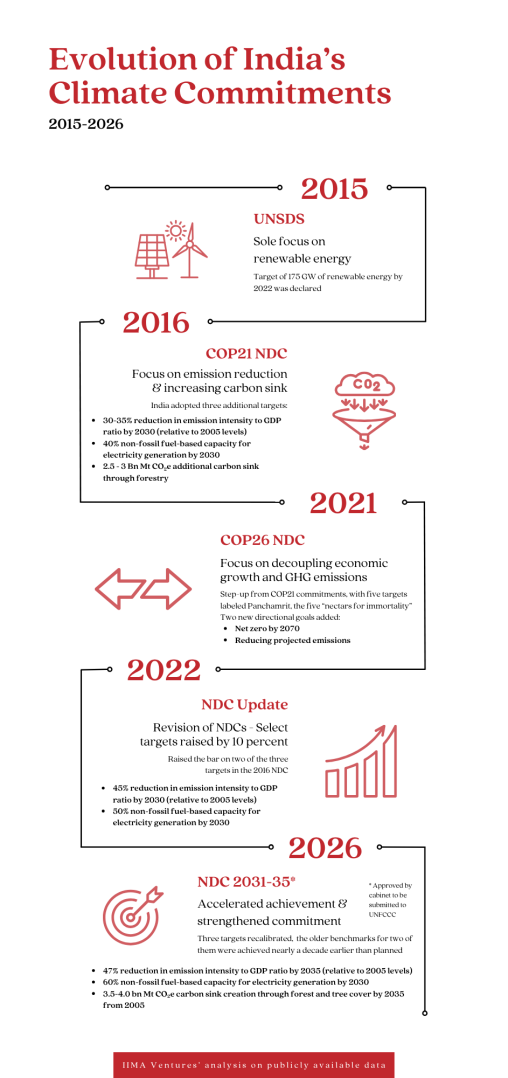

In light of this impossible position, India has, over the past decade, made increasingly bold climate commitments on the global stage and undertaken sustained domestic efforts to achieve those goals. From a singular focus on renewable energy to a cross-sector net-zero transition, these commitments have evolved and strengthened over time.*

Green energy has always been the loudest part of India’s climate story, beginning with a target of 175 GW of renewable energy (RE) and evolving into the ambitious goal of 60% non-fossil fuel capacity in electricity generation. But what do these targets actually unlock for founders and what do they leave unsaid?

Energy Infrastructure

India boasts an impressive non-fossil fuel installed capacity of over 50% (~283.46 GW) as of 31 March 2026. But even a cursory look into the country’s energy generation mix paints an entirely different picture. Renewable energy accounts for less than 30% of the total energy mix, indicating a continued dependence on coal (~70%) and other non-renewable sources. This gap points to significant infrastructure challenges that remain unsolved. Technologies and solutions that enable higher integration of RE, such as smart grids, energy storage, energy generation and demand forecasting, continue to be focus areas that need innovative startup founders and private-sector participation. Companies like Prescinto (acquired by IBM), SmartMeter, Aegeus Technologies, Aerem and Edgegrid are helping make RE more accessible, affordable and efficient.

Industrial Decarbonisation

India’s target of a 47% reduction in emission intensity^ by 2035 directly competes with its aspirations for manufacturing-led economic growth. This year’s budget (2025-26) alone targets an increase in manufacturing’s GDP share to 25% by 2035. As the second largest contributor, industrial emissions account for 22% of India’s total emissions. To chase both these goals simultaneously, India will need to rethink how industry functions from the ground up. Fuels, materials and processes will all need to undergo a fundamental shift without compromising overall production.

Green hydrogen is emerging as the fuel of choice for hard-to-abate sectors such as steel, chemicals, and fertilisers that can’t simply be electrified. Startups are building solutions to unlock greater efficiency and cost reduction in existing infrastructure. One such startup, Newtrace, claims to have reduced energy consumption during hydrogen production by up to 9.5kWh/kg H₂. It has deployed its membrane-less electrolysers with India’s leading hydrogen producers, including Bharat Petroleum Corporation Ltd. (BPCL) and Oil & Natural Gas Corporation (ONGC). However, while the ambition is real, so is the gap: as of August 2025, less than 3% of the announced green hydrogen projects are operational.

Startups are repurposing industrial waste into low-emission or carbon-neutral materials, such as cement and bricks, turning one industry’s waste into another’s raw material. Our portfolio company, Angirus, uses its proprietary technology to make bricks from 100% recycled waste material, including 20% plastic waste. In 2024-25, India utilised ~98% of fly ash generated across power stations in diverse applications, including roads & flyovers (32%), cement (27%), and bricks & tiles (14%) among others.

At the process level, technologies like carbon capture at source and waste heat recovery are nascent but necessary. Recognising this, in May 2025, the Department of Science and Technology undertook a collaborative industry-academia initiative, setting up five Carbon Capture and Utilisation (CCU) testbeds in the cement sector. This first cluster of testbeds has seen participation from industry giants such as JK Cement, JSW Cement and Ultratech Cement and from academic institutions such as IIT Kanpur, IIT Bombay, IIT Tirupati, IIT Madras, BITS Pilani and IISc, with additional industry stakeholders. The policy and the industry are set up for experimentation and innovation, but the startup ecosystem is yet to catch up.

These cumulatively represent the kind of deeptech bets that are long on timeline but critical for India.

Carbon Sinks and Accounting

Carbon sinks play an integral role in emission mitigation, and for India, they represent an offset of about 18% as of 2020. India aims to expand its existing carbon sinks to 3.5 to 4 billion tonnes of CO2e through forests and tree cover by 2035. But the foundational calculations behind this have been contested for years and by many experts, including former civil servants. The Forest Survey of India counts plantations, mango groves and monocultures as part of tree cover alongside natural forests. The core problem isn’t just that the numbers are disputed; it is that we barely have the tools to get them right, especially at the resolution and frequency a national climate commitment demands. This is where deeptech plays a role: satellite-based forest carbon monitoring, LiDAR and remote sensing for biomass quantification and AI models that turn satellite data into verified carbon accounting. Beyond verification, credible science is what unlocks the opportunity in domestic and international carbon markets. Building that science to back these solutions is both a climate imperative and a significant market opportunity.

Beyond Mitigation

In a country like India, where the impacts of climate change are already a lived reality, adaptation deserves a sharper focus from policy and innovation. The National Action Plan on Climate Change (NAPCC) has recognised adaptation as a priority, yet energy-efficient cooling, resource optimisation, water efficiency, heat-resilient construction and early warning systems are all deeply technical solutions that remain massively underbuilt. India’s residential electricity demand for ACs alone is expected to increase ninefold by 2050. Companies like SmartJoules and SustLabs are enabling energy efficiency across commercial and residential settings. Already a water-stressed nation, India is anticipated to become water-scarce with per capita water availability dropping to around 1100-1200 m3 by 2050. VayuJal Technologies, Uravu Labs, and INDRA are among the few companies that are addressing this critical national challenge. India is also likely to account for 40% of global job losses (34 Mn) from heat stress by 2030, affecting productivity and living conditions. Sukoon is attempting to address this problem with wearables that adapt to harsh climate conditions and provide relief to outdoor workers. However, a heat stress startup ecosystem in India barely exists. These are not niche problems; they characterise the daily reality of running a business, cultivating land, or simply living in an Indian city today.

India’s climate story is still being written. Our analysis revealed that, out of nearly 3000 climate tech startups founded since 2014, about 800 remain active. These startups cumulatively raised around USD 6 billion (March 2025). Companies like Ola Electric and Ather have set benchmarks for climate tech companies reaching public markets. In 2025, AltCarbon, a Carbon Dioxide Removal (CDR) company, raised a USD 12 million seed round, indicating continued investor interest in the sector. Yet the ecosystem continues to face a valley of death in growth-stage funding. The majority of venture capital deals have been concentrated in the early stages, with less than 3% of all climate tech startups raising a Series A+ round. Many government incentives and initiatives remain exclusionary for startups and only benefit legacy players.

The real task will be to keep growing the economy and decarbonise at the same time. It has been established that energy consumption is directly proportional to GDP. We are thus optimising for an ambitious outcome in a heavily constrained environment. However, complexity has always been where the most consequential companies get built and India’s most fearless founders know it.

*As of the publication of this blog (5 May, 2026), India’s updated NDCs have received cabinet approval and are awaiting formal submission to the UNFCCC.

^Emissions intensity measures the amount of GHGs released per unit of activity or output, in this case GDP.

^Authored by Shailaja Shukla Williams & Gaurav Khemchandani.